Colin Read • February 12, 2023

Deep Think Until it Hurts - February 12, 2023

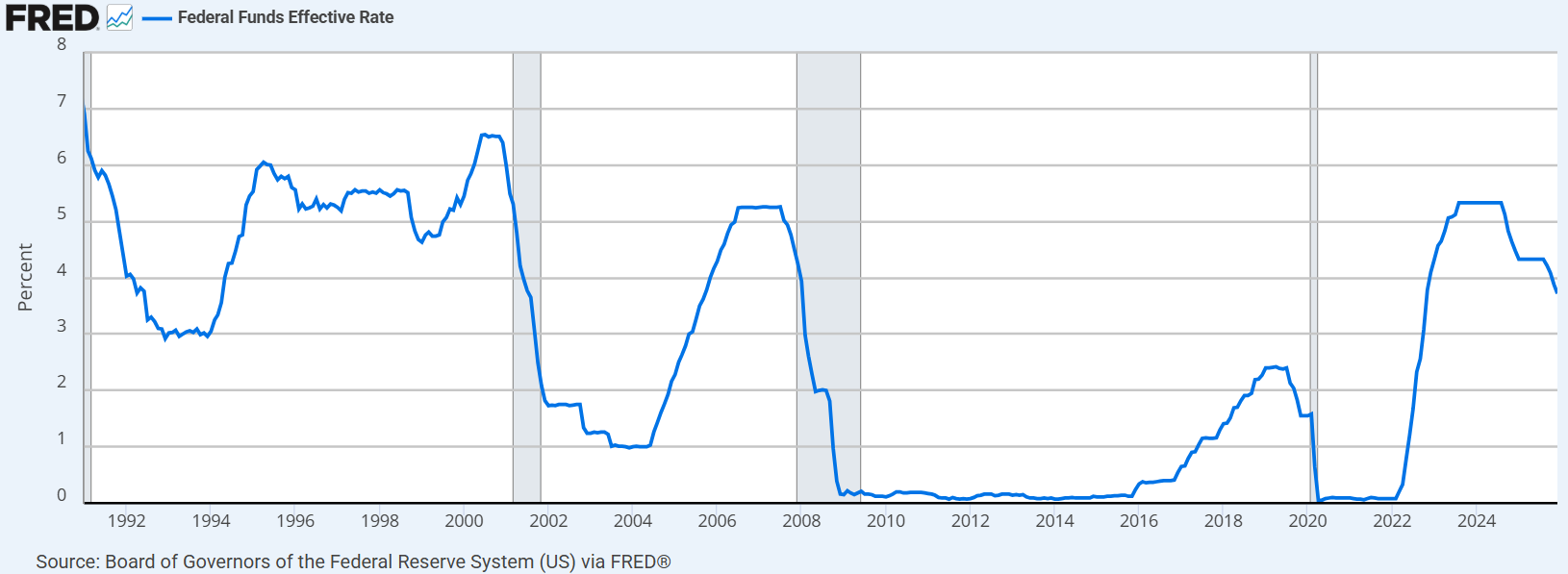

This economic era is perhaps the most vexing since the Great Depression. We have documented in this blog the missteps and failed opportunities of the Federal Reserve to stay ahead of the curve and prevent the inflation that reared its ugly head as people started to come outside and go off to work again.

Inflation makes difficult the planning and contracting of companies and erodes the pocketbook of those who live on fixed income and those least advantaged in our economy. We discussed here the reasons why the Covid post-quarantine era would likely generate inflation as supply could not respond to latent consumer demand. We advocated for a response from the Federal Reserve to temporarily institutionalize such price inflation through wage inflation, and we noted the importance of federal fiscal policy to straighten out kinks in the supply chain.

And, we documented how these cautions went unheeded until far too late. However, we note that, for the last half year or so, the forces of inflation have essentially abated. We also went through two successive quarters of GDP decline, which typically would constitute a recession.

However, the National Bureau of Economic Research did not call an inflation, and we did not see the typical rise in unemployment that usually accompanies such a decline in economic output.

The reason is not too difficult to see. It all comes down to a force that saved us from calling a recession, will likely allow us to experience a soft landing following the inflation and the Fed’s policies of late, and may also bode policy challenges in the future.

This new phenomenon is the most significant restructuring of labor markets since the mass exodus of manufacturing jobs in the 1970s and 1980s.

Two phenomena are occurring, one with potential long term consequences. If we look at the trend in the labor force over the past quarter century, we see that the Great Recession that ended the first decade of this century resulted in a greater than normal fall in the number of people who withdrew from the labor force. Some withdrawal is normal, but the loss of workers was more dramatic than normal around 2010. This fall coincides exactly with the first baby boomers attaining retirement age, and also then explains the reduced upward trend in the labor force and lower labor participation rate among our population ever since.

Such a lower labor participation rate is problematic since someone must still produce the goods and services these retirees need, and for a longer life expectancy than before. Let us assume that greater mechanization and efficiency will provide for this necessary supply despite the smaller labor force.

The greater problem is what happened next. Even if we anticipate slower growth of the labor force as our population grows but our baby boomers continue to retire for about another ten years, we are still missing about four million workers. If you extrapolate the labor force growth since the Great Recession but ignore the Global Pandemic, you notice that a good chunk of the labor force disappeared and have not since come back to the pre-pandemic trend line.

This disappearing labor force has two sides of the coin. The first is that a lot of people took their jobs and shoved it, and won’t go back. They have become a cadre of early retirees, gig economy workers, survivalists, and those who have reevaluated their priorities. That is the supply side. But, on the demand side, and the reason why employers have not been willing to offer sufficient wages to reengage a good chunk of the labor force is because of economic restructuring.

We have learned to work from home, work without traveling, and work smarter with fewer people. Innovations such as ChatGPT will accelerate the inevitable path toward a more laborless economy. For some applications, Artificial Intelligence (AI) is already superior to natural intelligence, and is certainly much cheaper.

This transition to a structurally different economy is just beginning to get rolling. It will mean what we have already seen - a reduced pressure for wages to keep pace with inflation, a continued pattern of labor force withdrawal, especially among middle age and older males, and reduced aggregate demand as more income becomes concentrated in the pocketbooks of those who benefit from reduced labor costs but who are sufficiently wealthy that they do not need to consume that additional wealth earned as the wealth of others declines.

Some argue that this wealth is ultimately reinjected into the economy through the stock market. It is true that such a structural shift results in increased forces for asset prices to rise. However, a more highly valued stock market does not translate into more spending if those becoming even wealthier are still not spending that wealth.

I stated earlier that this phenomenon, which explains what seems to be a dramatic departure from traditional economics, has public policy ramifications. Once we manage to figure out that the relationship between production and demand is experiencing a structural change, we will realize that something must move income back into the pockets of consumers. Ideas such as a Guaranteed Annual Income may warrant further exploration, but it would have to be accompanied with massive increases in the tax rate of the upper middle class and the wealthy class. Certainly, a national debt that has ballooned from $8 trillion to $32 trillion in just 15 years cannot further burden our children through income supplements without significant income redistributions as well.

The other question is education. If we move to a more laborless economy, what do we do with our next generation of workers? Certainly, automation will replace many low education jobs, but AI that can write a legal brief better than many junior lawyers, code better than many software engineers, or diagnose an X-ray or MRI better than many doctors will also have profound ramifications on high skill jobs as well. We can continue to educate young people at a high rate, only to better prepare them for Starbucks jobs, but those jobs too may become automated.

These are things, like many of the topics in this blog, that aren’t talked about much. They are complex subjects with a lot of moving parts, and hence are not ripe for soundbites or ideal for the short attention spans and even shorter time horizons of many of our politicians. They are something to deep think about though.