Colin Read • July 14, 2022

Emerging Economic Risks - July 17, 2022

Emerging Economic Risks - July 17, 2022

Nobody wants to hear “I told you so”, so let’s cut to the chase.

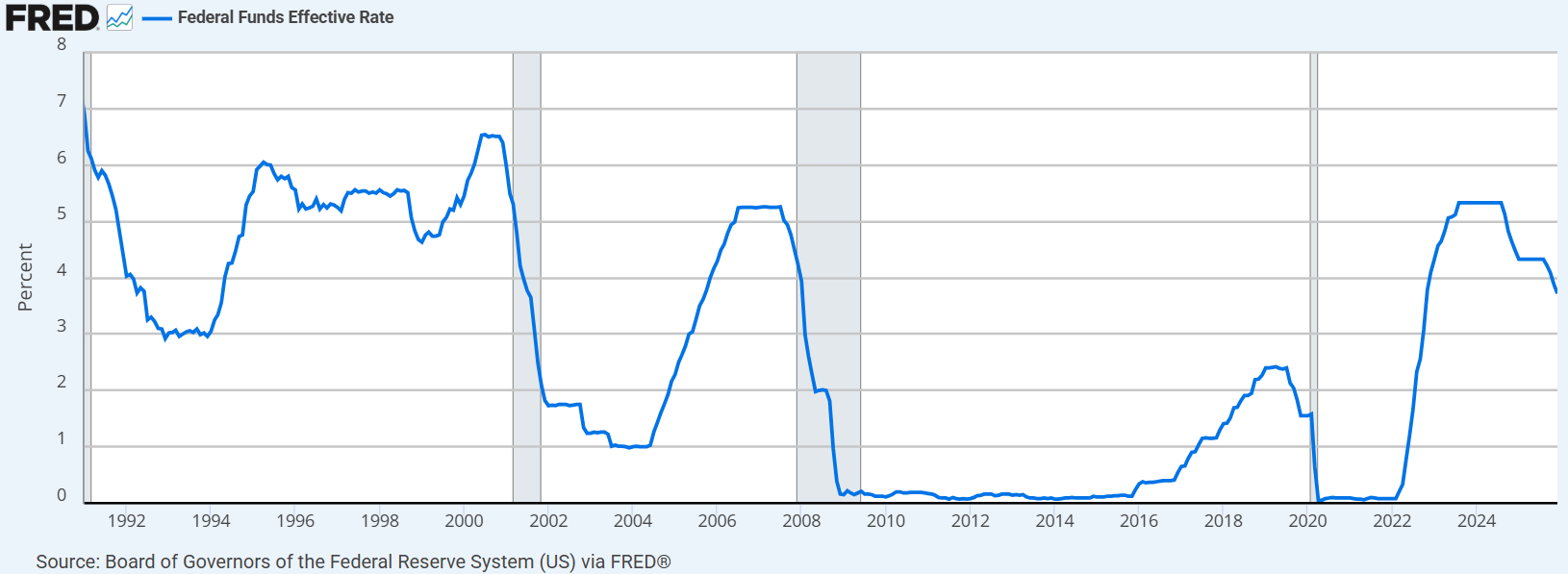

With inflation now exceeding 9%, what is the correct level for the Federal Reserve’s discount rate?

It is clear that too much spending is still chasing too few goods. When do people feel an urgency to spend? When the cost of holding money is higher than the cost of spending it.

The Federal Reserve does not set all interest rates, but they do set the rate for bank reserves and hence strongly affect banks’ willingness to lend. Of course, banks also raise funds from depositors, so they find that, as the Federal Reserve raises its interest rates, depositors also ratchet up their expectations on the interest rate they earn for their deposit.s

When we save, we are making a decision that sacrifices spending, the alternative to saving, in the hope that the interest accruing on deposits will afford even greater consumption later.

Aye, there’s the rub.

Let’s say the Fed gets the discount rate up to 4%, which remains a world away from the incredibly low 1.75% today, even after dramatic increases in the federal discount rate of late.

I calculate that if I put my money away for a year rather than purchase a consumer durable today, or a new electric car with lower operating costs, maybe after a few more discount rate jumps, I might earn 4% on my money. But, with the inflation rate now exceeding 9%, to delay such spending in an inflationary environment actually puts me 5% behind in purchasing power after a year.

In other words, the real, inflation-adjusted, interest rate is negative, at -5%.

Usually, the real interest rate in the US economy hovers around 3%. Our interest rates usually lead the inflation rate by that amount, rather than trail it by 5%. In other words, the Federal Reserve would have to increase the discount rate to low double digits in this inflationary environment, perhaps through historically unprecedented increases of 1% every month for the next year!

Only then will people make more rational decisions to stop chasing our tail. In an excessively low interest rate environment, one can’t afford to do the right thing and delay consumption and save, knowing that almost double digit inflation will quickly erode spending power.

So, people spend, which continues the cycle of too much spending chasing too few goods, with greater inflation the result. The greater inflation simply worsens this vicious cycle.

To make matters worse, the soaring dollar that suggests some of our trading partners may even be in worse shape just makes this vicious cycle worse. We find imports attractively priced when the dollar is strong, and hence we spend even more.

I’ve argued before that this inflation should not have been denied or minimized, and that there is no easy cure or soft landing. Accelerating inflation requires stiffer medicine than most are willing to administer. Talk of a soft landing, or blame directed at Putin are mere distractions designed to take our eyes off the inevitable and somewhat painful solution.

The fly in the ointment now is our low unemployment rate. That allows some to argue that, while inflation is the worst we’ve seen in forty years, the economy is humming along nicely. Really? Our low unemployment rate is a result of the fact that millions left the workforce over the COVID era and are unwilling to come back. If we calculated the unemployment rate based on what it would have been without COVID, the number of filled jobs versus the traditional labor force would translate into a high 5.5% unemployment rate.

In other words, the economy is not doing well. Using normal measures, we are in an early 80s style stagflation, or at least an early stage of it. Yet, the Federal Reserve has a lot of work cut out for it. Until the latent savings from government COVID largesse and recent wage increases are exorcized from the system, the Federal Reserve will have a difficult time gaining traction in its effort to slow down the economy. This time around there are just too many dangling objects to distract us or to allow us to too-easily conclude that the economy shall heal itself.